take rate

Смотреть что такое «take rate» в других словарях:

take-up — ˈtake up noun [uncountable] MARKETING the rate at which people buy or accept something offered by a company, government etc: • The bank has not announced targets but it will need high take up rates to justify its investment. * * * take up UK US… … Financial and business terms

take-up rate — noun The number of people, as a percentage of the total number eligible, who claim a benefit to which they are entitled or who accept an offer • • • Main Entry: ↑take … Useful english dictionary

rate — [n1] ratio, proportion amount, comparison, degree, estimate, percentage, progression, quota, relation, relationship, relative, scale, standard, weight; concept 768 Ant. whole rate [n2] fee charged for service, privilege, goods allowance, charge,… … New thesaurus

rate tart — noun (informal) A person who frequently moves money between different savings accounts in order to take advantage of the most favourable rates of interest. • • • Main Entry: ↑rate … Useful english dictionary

take up — vt to absorb or incorporate into itself <the rate at which the cells took up glucose> take up n … Medical dictionary

take-up — n [U] BrE the rate at which people accept something that is offered to them ▪ Take up for college places has been slow … Dictionary of contemporary English

take the pulse of — take (or feel) the pulse of determine the heart rate of (someone) by feeling and timing the pulsation of an artery a nurse came in and took his pulse ■ figurative ascertain the general mood or opinion of he hopped around the country to visit… … Useful english dictionary

Rate of profit — In economics and finance, the profit rate is the relative profitability of an investment project, of a capitalist enterprise, or of the capitalist economy as a whole. It is similar to the concept of the rate of return on investment. In Marxian… … Wikipedia

Rate equation — The rate law or rate equation for a chemical reaction is an equation that links the reaction rate with concentrations or pressures of reactants and constant parameters (normally rate coefficients and partial reaction orders).[1] To determine the… … Wikipedia

Rate of return — In finance, rate of return (ROR), also known as return on investment (ROI), rate of profit or sometimes just return, is the ratio of money gained or lost (whether realized or unrealized) on an investment relative to the amount of money invested.… … Wikipedia

rate — Synonyms and related words: VAT, abuse, account, ad valorem duty, admonish, alcohol tax, alphabetize, amount, amusement tax, analyze, antecede, anyhow, anyway, apportion, appraise, appreciate, arithmetical proportion, arrange, assay, assess,… … Moby Thesaurus

Зачем нужны продакт-менеджеры в финтехе

Все знают, что продакт менеджеры делают в е-коммерс: оптимизируют воронку и придумывают «как сделать сайт таким же удобным для покупок, как домашние тапочки для похода на кухню ночью». Но сегодня почти любая уважающая себя компания, которая так или иначе присутствует в диджитале, начинает внедрять продуктовый подход с свою работу: телеком, банки, страховые… даже фастфуд.

Под катом Александр Окулов из компании ID Finance рассказывает о том, какие вопросы стоят перед продактами в финтехе, цифровом с рождения, но много взявшем от своих родителей, традиционных банков и финансов. В финтехе, как правило, бизнес строится вокруг продукта и везде сплошной agile, а про «водопад» слышали лишь те кому за 30 и кто успел поработать в компаниях-динозаврах.

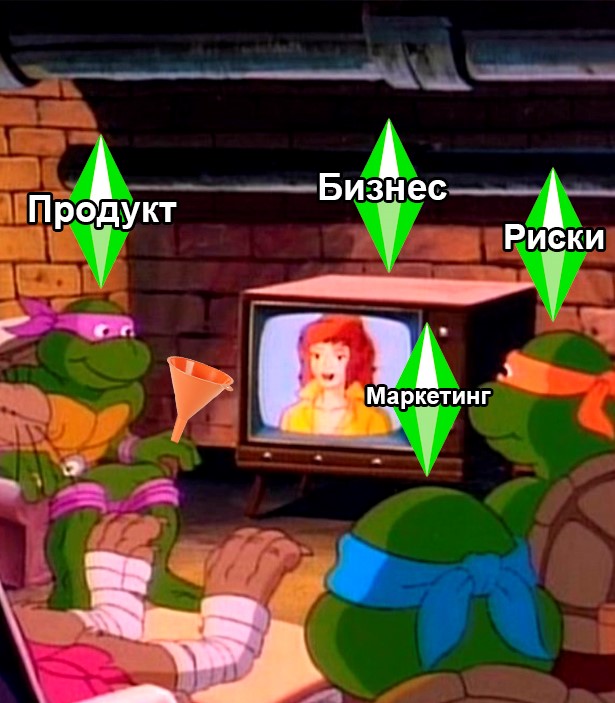

Пара слов о трех черепахах

Продукт в финтехе это лишь одна из этих черепах, которая как и в е-коммерс несет на себе воронку. Еще две черепахи — это маркетинг и риски. Маркетинг приводит трафик в воронку, а риски ставят фильтры в его горлышке. Если будет хромать одна из трех черепах, бизнес может накрениться и дефолтнуть.

Это ключевое отличие от диджитал компаний, где часто есть только продукт и маркетинг продукта. Почти половина вопросов, которые приходится решать той или иной черепахе — находятся на стыке ответственности двух других и поэтому их приходится решать совместно в команде, много обсуждать и много тестировать.

Отсюда очень важная особенность продуктовых вопросов в финтехе: нужно понимать сленг коллег, в первую очередь из рисков, зависимости между смежными KPI и как изменения одного приводят к изменениям в другом.

Давайте начнем со слэнга, а потом посмотрим несколько кейсов, когда продактам нужно взаимодействовать с прагматичными риск-математиками и мечтательными маркетологами.

Сленг кредитных рисковиков

AR — approval rate. Соотношение одобренных кредитов к поданным заявкам.

IR — issue rate. Соотношение выданных кредитов к поданным заявкам (бывает так, что компания одобрила заем, но он не был выдан: банк отклонил транзакцию или сам заемщик передумал).

RR — recovery rate. Соотношение входящего денежного потока к исходящему.

NPL — non performing loan. Соотношение количества “не платящих” клиентов к тем, кто оплачивает вовремя. Иными словами просрочка.

NPL2, NPL15, NPL30, NPL90 — non performing loan after 2,15,30,90 days. Соотношение NPL взятое через 2,15,30,90 дней после даты планового поступления.

FPD, SPD, TDP — first (second, third) payment default. Термин актуальный для кредитов с аннуитетными платежами, это соотношение количества “не платящих” первый (второй, третий) платеж к тем, кто оплачивает этот платеж вовремя.

Как вы уже, наверное, догадались, все эти показатели выражаются в процентах и многие из них актуальны для всей банковской индустрии, правда называться они могут по-разному. Например даже у нас в компании у финансистов есть своя странная терминология, которую они используют. Ну и смотреть эти показатели нужно в разрезе винтажей. Что? Да, я тоже раньше называл их “купажами” и не мог понять зачем финансисты извратили всем известную терминологию когортного анализа. Если коротко, то в финансах винтаж

когорта, только когорта клиентов, а не кредитов. Чтобы расставить все точки над рисками, надо сказать что самым важными показателями являются RR, NPL и AR.

Немного про recovery

Продуктовый мир живет в парадигме юнит экономики и LTV (life time value, жизненный цикл клиента) и мало кто слышал про recovery, но на самом деле они очень похожи. И тот и другой про то, сколько ты зарабатываешь с определенной группы. Но вот в чем отличия:

Представьте себе кредитный продукт длительностью в 12 месяцев. В течении года вы каждый день выдаете эти 12-месячные кредиты. Как понять сколько вы заработали по результатам года, ведь многие могут не вернуть кредит, многие могут закрыть кредит раньше срока и т.д.? Для этого нужно ждать пока пользователь заплатит по этим кредитам до 3-4 платежа (“дать вызреть”) и затем на основе статистики каждого винтажа вы сможете спрогнозировать recovery вашего портфеля. Посчитать выручку дальше уже несложно.

Зачем продакту нужен этот показатель? Очень часто, когда вы тестируете бизнесовые изменения, а не UI/UX (юзабилити) который проще померить в конверсии, то основным “мерилом” эффекта будет именно recovery, показатель отражающий удельное повышение вашего заработка.

NPL — это второй по важности показатель. Он применим к винтажам и к портфелю целиком. Это показатель характеризует пользовательский трафик, который проник в вашу воронку и приносит вам деньги. И чем он ближе к 0% — тем лучше, 0% означает что все клиенты платят по кредитам. Так, конечно же, не бывает в реальной жизни. Всегда есть те пользователи, которые не платят за свою подписку в Netflix. Но Netflix может просто отключить им доступ к своему контенту. Мы же не можем забрать выданные деньги назад, поэтому для нас это потери, которые сильно влияют на экономику как продукта, так и всего бизнеса. И примерно каждый второй тест, который запускают продакты и маркетинг требует оценки изменения NPL.

AR/IR. Все мы знаем, как работают банки, они нас “скорят”, прогоняют собранные про нас данные через свои модели оценки рисков, ставят нам баллы и определяют “хороший” или “недостаточно хороший” клиент перед ними. Уровень одобрения это результат работы скоринга. Чем более продвинутые скоринг-модели у компании, тем больше клиентов она сможет получить на рынке, и тем больше будет отдача от инвестиций в привлечение клиентов.

Надеюсь вы понимаете, что обозначенные риск-показатели это лишь верхушка айсберга.

Маркетинговые показатели

Они очень похожи на продуктовые, важно то, как отделы договаривается по зонам ответственности внутри компании. Как правило CR (конверсия) и retention — это совместные продуктово-маркетинговые показатели, а вот стоимость привлечения клиента уже чисто маркетинговый показатель.

Главная цель продактов

Как я уже говорил, одна из важнейших зон ответственности продактов в ID Finance — это воронка: процесс, когда пользователь становится нашим клиентом заходя на наш сайт. Воронки в разных сервисах могут быть технически устроены по разному, но цель продактов всегда одинакова: минимизировать издержки (funnel costs: APIs, comminications, processing, identification, OCR and other) и максимизировать количество пользователей, добравшихся до горлышка — CR (конверсию). Тут и решение вопросов дизайна и UI, UX (юзабилити), API интеграций (в наших воронках много интеграций со сторонними сервисами), возврат брошенных регистраций (они же abandoned basket в онлайн шоппинге), вопросы безопасности, моделирование кейсов и просчет экономики улучшений — все это в борьбе за драгоценные процентные пункты конверсии.

Однако, конвертнуть пользователя с сайта — это лишь начало. Пользователей, ставших обладателями ценного звания нового клиента, предстоит еще обернуть в повторных клиентов. Тут работает стандартный тандем маркетинга и продакт менеджеров — вместе мы придумываем как это сделать и следим за retention (у нас

90%). В ход идет весь арсенал директ-маркетинга и коммуникаций, разработка привлекательных продуктовых предложений (но с хорошей экономикой), бонусные программы, скидочные программы и т.п. И, конечно же, через пару лет после старта проекта повторные пользователи становятся основным источником прибыли и мы о них активно заботимся и думаем.

Экономика проекта

Экономика — это самая интересная и самая сложная часть в разработке продуктового функционала в финтехе. Тут мы следим за average check (средним чеком), и за LT/LTV. При тестировании и проработке продуктовых особенностей необходимо отследить весь ворох показателей. Именно это сложнее всего, потому что мы частично на поляне “рисков”, владельцев показателей (просрочки и recovery), которые на самом деле не любят рисковать.

Они будут стараться минимизировать доли трафика на тестовые ветки, придумывать множество причин почему нужно осторожничать. Нужно отдать им должное — они очень часто оказываются правы, математики все-таки. И компромисс — это то, что помогает найти золотую середину между рискованностью нашего MVP и минимизацией возможных потерь при фейле. Тесты в области экономики продукта довольно долгие, но если тест оказывается успешным, то может принести хорошие дивиденды продукту и бизнесу.

Бизнес у нас непростой и без продактов в финтехе никак. Нужно быть техническим спецом, чтобы общаться на одном языке с dev командой и поставить задачу на разработку, нужно отлично понимать бизнес, чтобы заниматься разработкой и тюнингом продуктов, и нужно быть менеджером, чтобы заставлять все вокруг двигаться в нужном темпе.

В следующей статье расскажу зубодробительные кейсы про то, как ваша классная продуктовая фича может взвинтить и RR и NPL одновременно, и про то как можно улучшать CR одновременно снижая, например, AR.

take rate

1 take rate

2 take (one’s) pulse rate

3 take-off rate

4 take pulse rate

5 take-off rate

6 take-up rate

См. также в других словарях:

take-up — ˈtake up noun [uncountable] MARKETING the rate at which people buy or accept something offered by a company, government etc: • The bank has not announced targets but it will need high take up rates to justify its investment. * * * take up UK US… … Financial and business terms

take-up rate — noun The number of people, as a percentage of the total number eligible, who claim a benefit to which they are entitled or who accept an offer • • • Main Entry: ↑take … Useful english dictionary

rate — [n1] ratio, proportion amount, comparison, degree, estimate, percentage, progression, quota, relation, relationship, relative, scale, standard, weight; concept 768 Ant. whole rate [n2] fee charged for service, privilege, goods allowance, charge,… … New thesaurus

rate tart — noun (informal) A person who frequently moves money between different savings accounts in order to take advantage of the most favourable rates of interest. • • • Main Entry: ↑rate … Useful english dictionary

take up — vt to absorb or incorporate into itself <the rate at which the cells took up glucose> take up n … Medical dictionary

take-up — n [U] BrE the rate at which people accept something that is offered to them ▪ Take up for college places has been slow … Dictionary of contemporary English

take the pulse of — take (or feel) the pulse of determine the heart rate of (someone) by feeling and timing the pulsation of an artery a nurse came in and took his pulse ■ figurative ascertain the general mood or opinion of he hopped around the country to visit… … Useful english dictionary

Rate of profit — In economics and finance, the profit rate is the relative profitability of an investment project, of a capitalist enterprise, or of the capitalist economy as a whole. It is similar to the concept of the rate of return on investment. In Marxian… … Wikipedia

Rate equation — The rate law or rate equation for a chemical reaction is an equation that links the reaction rate with concentrations or pressures of reactants and constant parameters (normally rate coefficients and partial reaction orders).[1] To determine the… … Wikipedia

Rate of return — In finance, rate of return (ROR), also known as return on investment (ROI), rate of profit or sometimes just return, is the ratio of money gained or lost (whether realized or unrealized) on an investment relative to the amount of money invested.… … Wikipedia

rate — Synonyms and related words: VAT, abuse, account, ad valorem duty, admonish, alcohol tax, alphabetize, amount, amusement tax, analyze, antecede, anyhow, anyway, apportion, appraise, appreciate, arithmetical proportion, arrange, assay, assess,… … Moby Thesaurus

Why the Take Rate Is So Important in E-Commerce

Taking a cut for services is a key profit driver for many companies.

What take rates look like in online marketplaces

For online marketplaces like what Amazon and eBay offer, the take rate refers to the fees and commissions that the companies collect on sales by third-party sellers. For eBay, those fees typically take the form of initial listing fees for offering goods and services on its marketplace in the first place, as well as final value fees that the e-commerce specialist collects after a successful sale.

Image source: Getty Images.

The key issue with take rate in online marketplaces is the tug-of-war between maximizing profit and keeping customers within the network. eBay has traditionally sought to move its take rate higher, boosting final value fees and taking a bigger piece of its sellers’ sales. Yet as it has done so, eBay has opened the door to competing marketplace services, and the rise of companies like Etsy has shown that raising take rates too high can enable competitors to undercut based on price and lure cost-sensitive users away.

In assessing the health of Amazon, eBay, and other marketplaces, it’s valuable to look at gross merchandise volume and segment profitability. Volume growth is important to ensure that the network is healthy, but the ratio of profits to volume is directly proportional to the take rate, and growth in profits is necessary to show that the company is finding the optimal take rate to balance income and revenue.

What take rates look like for payment networks

What take rates look like for website analytics

Finally, take rate has a different meaning for marketing activity, including that done through e-commerce. Take rate reflects the fact that a great deal of internet marketing happens in multiple stages, where the first goal is to get a customer to click on an ad, and the next is to convince that customer to buy a product. The take rate in this case refers to the percentage of customers who click on the ad, in contrast to the conversion rate, or percentage of customers who not only took the ad but actually bought the product.

In general, a high take rate is good, but it’s essential that conversion rates be strong as well. For marketers, a high take rate and a low conversion rate can be the worst of all worlds in e-commerce. Often, marketing costs are based on the number of people clicking through, and it’s then up to the company to convince those people to buy a product. By contrast, a lower take rate can be better if it doesn’t hurt conversions, because it will cost less to drive the same amount of final sales.

Take rate gets used in a variety of contexts, and it’s important to know what each specific instance means. In general, though, the best e-commerce companies are those that sustain high take rates while keeping competitors at bay.

Take Rate: Its Role in the eCommerce and Fintech Industries

Today’s marketplaces and finance industries are changing at a rapid pace. The rise of eCommerce and Fintech disrupts the way we buy and sell merchandise, car rides, banking, and groceries. With that rise comes new terms that help us determine how profitable these companies are, plus how to define their pricing power.

The take rate has been around for a while, but the term has risen in popularity more recently with the rise of companies such as Paypal, Airbnb, Shopify, and Etsy. But companies such as Visa, Mastercard, and American Express have used these terms to define their revenues for decades.

Defining the take rate and understanding its importance in Fintech and the online marketplaces helps investors translate how these businesses, such as Amazon, eBay, and Paypal generate revenues and grow their user bases.

For example, recognizing the strength of the online marketplaces, Paypal purchased Honey.com in 2019 to capture more take rates via the marketplaces and move beyond processing payments.

In today’s post, we will learn:

Okay, let’s dive in and learn more about the take rate.

What is a Take Rate?

A take rate is a fee charged by a processor or merchant on a transaction, either by a third-party ala Amazon or by a service provider ala Paypal. Those take rates are the primary source of revenues for companies such as Paypal, Shopify, Etsy, eBay, and many more.

A simple example of the formula to determine the take rate for a company is to divide the revenue generated from those fees by the total merchandise volume or transaction volume, more on this in a moment.

The take rate multiplied by the total volume transacted on the platform generates revenue for the company. For example, one of the strengths of Shopify is the ability to keep customers on their platforms by allowing a two-sided transaction. As a result, customers can shop and buy on Shopify’s platform, which generates revenue for the company from the fees to process the transaction. Also, the fees it generates from the merchants selling their wares on the platform.

The take rates differ across platforms; for example, Amazon and eBay charge anywhere between 5-20% on their marketplaces, which are fees they collect from their third-party sellers which generate revenues for Amazon and eBay.

Service providers such as Airbnb and Uber charge between 15-25% fees for their platforms, which they charge to the service provider, driver, or homeowner, to generate their revenues. These higher fees are a result of the lower transaction activities, compared to Shopify, for example.

The higher transaction frequencies such as online merchants, Shopify, Amazon, and Etsy can charge much lower take rates than Airbnb, which has far lower transaction frequencies.

More conventional businesses like Walmart don’t work with take rates; their revenues are more old-school. Instead, their income statements reflect the flow of buying inventory, stock shelves, paying employees, and customers depleting the store’s inventories.

A company like Shopify is a different model. They sell and process their payments through an online portal that allows the customer and merchant to transact virtually, and all the fees from buying and selling flow to Shopify as their revenue.

To consider evaluating a company like Shopify, Etsy, Airbnb, Uber, or Paypal, we need to consider the Gross Merchant Volume (GMV) or Gross Payment Volume (GPV) to understand the generation of revenues. Considering both the GMV and GPV helps us understand how much activity occurs on their platforms, and the take rate tells us how much revenue they can capture from that volume.

The higher the volume on the platform, the more ability to grow revenues, which is why we need to look for GMV or GPV when searching the financial statements. Considering both those metrics, take rates, and revenues will tell you how well the company performs.

How is the Take Rate Calculated?

The calculations to determine the take rate for both service providers and merchant providers is simple division. The bigger challenge is finding the information in the company’s financials to make the calculations.

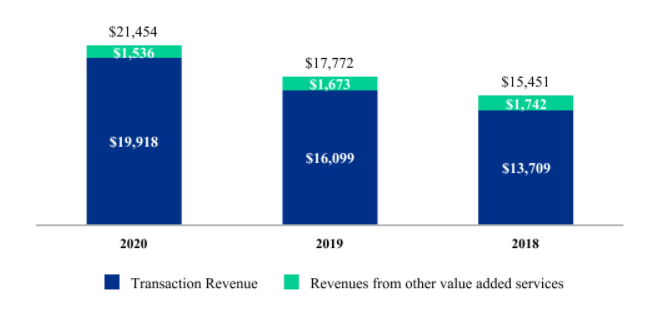

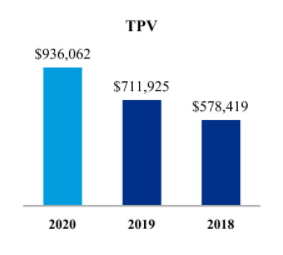

First, let’s look at the take rate for Paypal. I will use the data from the latest 10-k, dated December 31, 2020. I found the information using the “ctrl-f” function to search for Total Payment Volume (TPV). I found both of these charts, which will help us calculate the take rate.

Total payment volumes:

To determine the take rate for Paypal, we divide the net revenues by the total payment volume:

Take rate = net revenues / total payment volume

Let’s look at Paypal’s take rate over the last three years:

Okay, let’s look at one from the merchant side. We will try Shopify next, and using their latest 6-f, dated April 28, 2021, we can determine what Shopify’s take rate is for their merchant processing segment.

To determine Shopify’s take rate, we find that the company’s merchant revenues for the quarter were:

That was an increase from the 1.62% take rate in the first quarter of 2020, which was:

Now, let’s look at the take rate for Uber, and we will use the numbers from the latest 10-k, dated March 1, 2021, and we will separate the main three drivers of revenue for the company by their take rates:

After all of that, I think we understand how to calculate the take rate for any merchant processor and service company. The biggest issue is determining the company’s metric to track the volume of transactions across their platform.

Keep in mind the metrics, ratios, and numbers we are talking about at this time are non-GAAP numbers, which means that no company is under any obligation to track these numbers to help investors determine the profitability or drivers of growth.

The Importance of the Take Rate in eCommerce

Online merchants like Amazon and eBay collect their fees and commissions from their third-party sellers, tracking their take rates. For example, eBay collects fees for listing products and services on their website, plus the final fees they collect from a successful sale.

The key issue with the take rate in online marketplaces is the yin and yang between maximizing profits and keeping customers on the network. If a company tries to increase its take rate, as eBay has done by increasing its take rates and final fees to gain a bigger piece of the pie, but in doing so opened the door for companies such as Etsy to move in and offer lower fees and lure away the more cost-conscious customers.

When we look at the financial health of some of these online marketplaces, such as Amazon, Shopify, eBay, and Etsy, it is useful to look at the gross merchandise volume and the profitability of each segment.

Volume growth is important because the more users are on the platform, the greater the chances of revenue growth. And if the company can create more user value adds, they can keep users on the platform.

One of Shopify and Etsy’s strengths is keeping users on the platform and deepening the customer relationship by offering more products and functionality.

Focusing on the volume growth helps keep track of each company’s health, and tracking that volume growth will help you see if a platform is healthy.

But also tracking the ratio of profits to the transaction volume is directly proportionate to the take rate. By tracking the profit ratio, we can see that the company is finding the right balance between income and revenue.

Keep in mind that there is a difference between types of online marketplaces. For example, Amazon, eBay, Shopify, and Etsy offer third-party transactions on their platforms, which allows all of these companies to generate revenues from both the buyers and sellers of products. These are two-sided marketplaces and allow the platforms to grow their revenues quickly as the marketplace volumes grow.

That makes companies like Amazon and Shopify such strong business models and allows them to grow rapidly. Shopify also generates revenues from its subscription services or recurring revenues from its merchants; it’s a brilliant business model.

Take Rate and Fintech

The take rate idea is the same for Fintech. Companies such as Paypal, Square, Global Payments Network, Stripe, and Visa all take a percentage of each transaction in exchange for easing the transfer of money from a buyer to the seller.

That take rate for the transaction is 3%, but it doesn’t all go to Paypal. Others are enabling the transaction that takes a cut of that percentage.

Below is a great example of how the whole process works via Paypal.

Visa and Mastercard are the two most dominant players in the fintech payment processing world. They operate the payment rails for all card processors; in other words, they are the gateway for all processors.

Neither company has actual credit cards or bank accounts; instead, they created a network that allows all payments to flow across that network between buyers, merchant processors, banks, and sellers.

Of course, they do charge a fee for this gateway, depending on the type of transaction. But by and large, these take rates are stable across the network and allow for stable processing across the networks. As of 2021, the average take rates for credit card processing are between 1.3% to 3.5%, depending on the type of transaction and network.

For merchants to accept credit card payments, they must agree to interchange fees (Visa and Mastercard), assessment fees, and processing fees. These fees get split up between the card’s issuing bank, payment network, and payment processor.

Those fees, although small on an individual basis, make up large amounts as the network grows. That is why payment processors such as Square and Paypal get so much attention, plus processors such as Square have started banks to help grow the unbanked revenues and allow for easier payment options.

Investor Takeaway

As we discovered, diving into the take rates for online marketplaces, service providers, and payment processors tells us a lot about the profitability and growth of the companies.

The competition and demand for these products and services grew exponentially during the pandemic, and many think that demand will continue long after, as habits and patterns become the norm.

The take rate calculation itself is quite simple. The biggest issue is determining what to compare that revenue to. It is important to analyze the company’s profit margin because those ideas are correlated.

Keep in mind that take rate, the gross payment volume, gross merchandise volume are non-GAAP numbers, so there is little standardization across the board. It might take a little hunting to find what you are looking for, but it is there if you look deep enough.

The take rate is also a great metric to track the strength of both the company’s website volume and pricing power. Paypal is a great example of a strong company with a growing base reliant on its platform to move money. As someone who worked in banking for a while, I know how sticky banking or money platforms can become, as it is painful to move.

As Paypal via Venmo becomes more relevant, it will grow the ability to continue to raise prices incrementally, which will grow its revenues.

These are all ideas and metrics to consider when analyzing online merchants, payment processors, service providers, or any company using online networks to conduct business.

And with that, we will wrap up our discussion on take rates.

As always, thank you for taking the time to read today’s post, and I hope you find some value in your investing journey. If I can be of any further assistance, please don’t hesitate to reach out.

Until next time, take care and be safe out there,